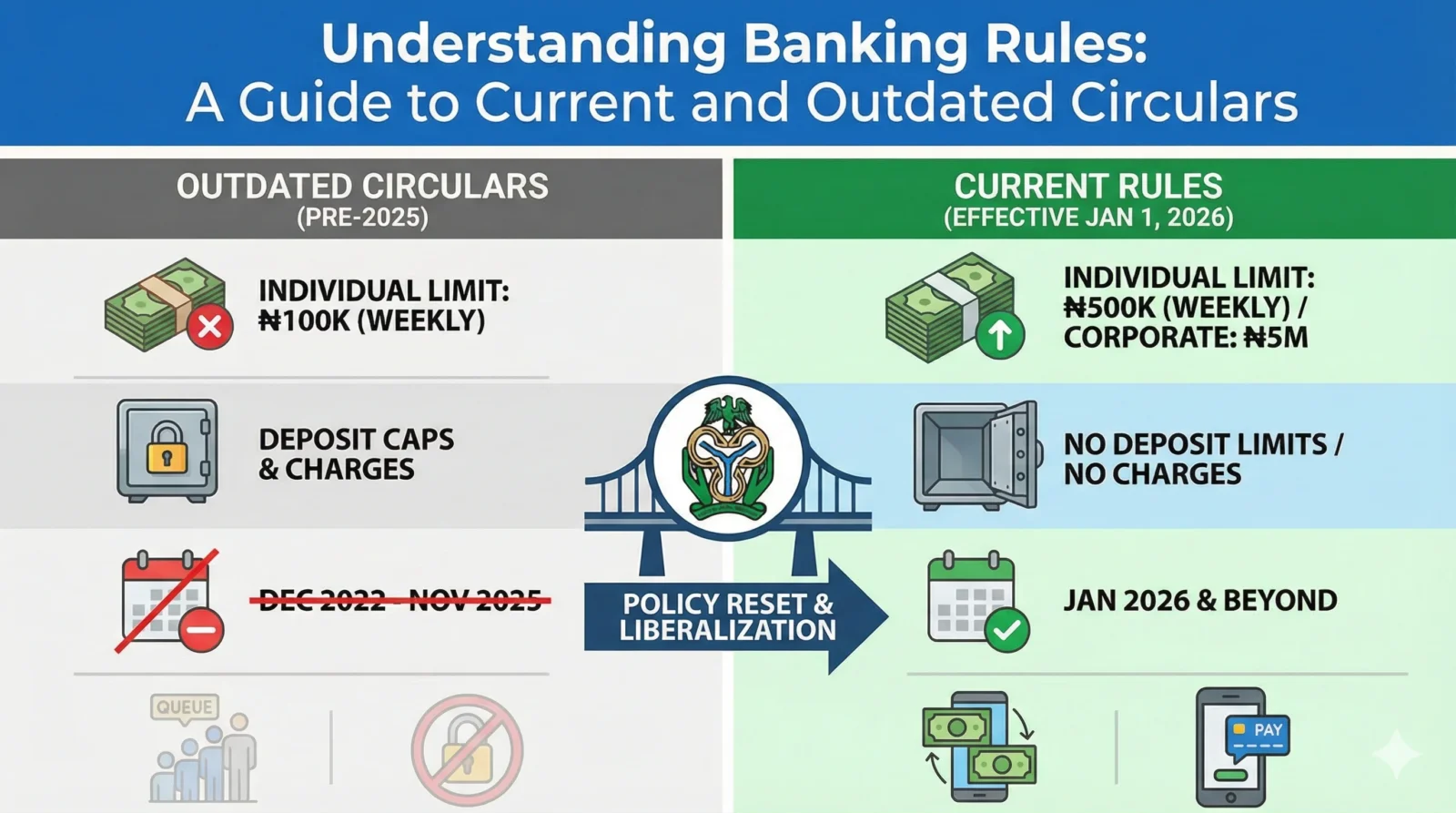

Imagine trying to navigate a modern city using a paper map from twenty years ago. You would miss new highways, get stuck on one-way streets that have changed direction, and be completely unaware of new developments. This old map is like an outdated banking rule, following it leads to confusion, inefficiency, and significant errors. Read on Nigeria Just Hit Reset on a Decade of Cash Policy: Here’s What Matters.

In contrast, a current banking regulation is like a modern GPS. It provides the most accurate, real-time information, guiding you along the correct and most efficient route. It accounts for all the latest changes to the landscape, ensuring you reach your destination safely and without issue.

The purpose of this guide is to help you understand the difference between these “old maps” and “new GPS” systems in the banking world. By examining official lists of active and outdated rules, we can see why this distinction is one of the most critical aspects of the financial industry. Now that we have a basic idea, let’s look at the official terms the banking industry uses for these “old and new maps.”

2. Defining the Key Terms: Superseded vs. In Effect

To navigate the world of banking compliance, you must first understand the language. Here are the core terms that define the status of a regulation.

- Circular: This is an official document issued by a regulatory body (like a central bank) to provide guidance, instructions, or mandatory rules to financial institutions.

- Not Superseded (In Effect): This means the circular is current, active, and legally binding. It is the “current rulebook” that banks must follow without exception.

- Superseded: This means the circular has been officially replaced by a newer one. It is an “archived rule” that is no longer in effect and must not be followed.

To reinforce understanding, this table directly contrasts the two states:

| Status | Meaning for a Bank |

| Not Superseded | This rule MUST be followed. It is the current law. |

| Superseded | This rule must NOT be followed. It has been replaced. |

To see how this works in practice, let’s examine the official lists of current and outdated circulars. As a compliance professional, your first question for any process should be, “Which circular is this based on, and is it still in effect?”

3. The Rules in Action: Analyzing Real Circulars

3.1. The Current Rulebook: Circulars That Are NOT Superseded

The following examples are from “Appendix 1 – List of Circulars That Are Not Superseded.” They represent the active rules that banks must follow today.

- Introduction of Three-Tiered Know Your Customer (KYC) Requirements (18-Jan-13): This rule likely establishes different levels of customer identification and verification that banks must perform.

- Deployment of Cash Activity Reporting Portal (CARP) to the Banking Industry (14-Oct-14): This circular most likely mandated the use of a specific digital portal for reporting cash transactions to regulators.

- Updated Penalty on Inappropriate Cash Disbursement Practices by DMBs (13-Dec-24): This regulation appears to revise the fines or sanctions for banks that do not follow the correct procedures for handling cash.

- Trainer’s Note: Note the future date on this circular. This signals a forthcoming rule change that compliance teams must prepare for, with enforcement beginning on or after this date.

3.2. The Archives: Examples of Superseded Circulars

These examples are from “Appendix 2 – List of Superseded Circulars.” They represent rules that are now outdated. Following these rules today would be a compliance failure because they have been replaced by newer instructions.

| Outdated Circular Title | Date | Why It’s No Longer Followed |

| Industry Policy on Retail Cash Collection And Lodgement (IITP/C/001) | 20-Apr-11 | This foundational policy has been replaced by a series of more specific and technologically current cash handling rules. |

| Re: Circular on Nationwide Implementation of the Cash-Less Policy | 20-Apr-17 | This was one step in a multi-year policy rollout and was superseded by subsequent circulars that further adjusted the implementation. |

| Re: Naira Redesign Policy – Revised Cash Withdrawal Limits | 21-Dec-22 | This was a time-bound directive issued during a specific monetary policy event (the Naira Redesign). It was naturally superseded once the event concluded and normal withdrawal limits were restored or revised. |

Seeing these old rules makes it clear that regulations change, which leads to the most important question: what are the consequences of not keeping up?

4. The Bottom Line: Why Compliance with Current Circulars is Non-Negotiable

Banking regulations are constantly updated for a simple reason: the financial world is always changing. New technologies emerge, new risks appear, and economic policies shift. The need for adaptation is obvious when looking at the archives. The source list of superseded circulars contains no fewer than five distinct updates to the “Cash-Less Policy” between 2014 and 2019, demonstrating a clear, iterative process of regulatory refinement.

Adhering strictly to current, non-superseded circulars is critical for several core reasons:

- Avoiding Penalties Regulators impose significant fines and other sanctions on banks that fail to comply with current rules. Following an outdated, superseded circular is a direct violation and will attract severe regulatory sanctions and financial penalties. For example, a bank that failed to implement the “Updated Penalty” circular by its effective date of December 13, 2024, would face immediate sanctions.

- Maintaining Operational Integrity Using old rules leads to incorrect internal processes. This can create security vulnerabilities, cause system errors, and result in inefficient operations that waste time and resources. Current rules ensure a bank’s operations are secure and aligned with industry standards.

- Ensuring Fair and Secure Banking Ultimately, regulations exist to protect customers and maintain the stability of the entire financial system. This is the very reason for foundational rules like the “Three-Tiered Know Your Customer (KYC) Requirements” from 2013, which are still in effect today to prevent fraud, money laundering, and other financial crimes.

5. Conclusion: Your Key Takeaway

The landscape of banking regulation is dynamic, not static. Circulars are continuously updated to address the needs of a modern economy. The key lesson is to understand the clear distinction between a superseded rule, which is an archived policy that must be ignored, and a not superseded rule, which is the current, active law. For any financial institution, staying vigilant and ensuring operations are based only on the latest circulars isn’t just good practice—it is a non-negotiable condition for maintaining its license to operate.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment